- Blog

- Sustainable Economic Systems

- Green Climate Fund

- 5 simple reasons to oppose HSBC and Credit Agricole at the Green Climate Fund

5 simple reasons to oppose HSBC and Credit Agricole at the Green Climate Fund

by Karen Orenstein, Deputy Director of Economic Policy

Donate Now!

Your contribution will benefit Friends of the Earth.

Stay Informed

Thanks for your interest in Friends of the Earth. You can find information about us and get in touch the following ways:

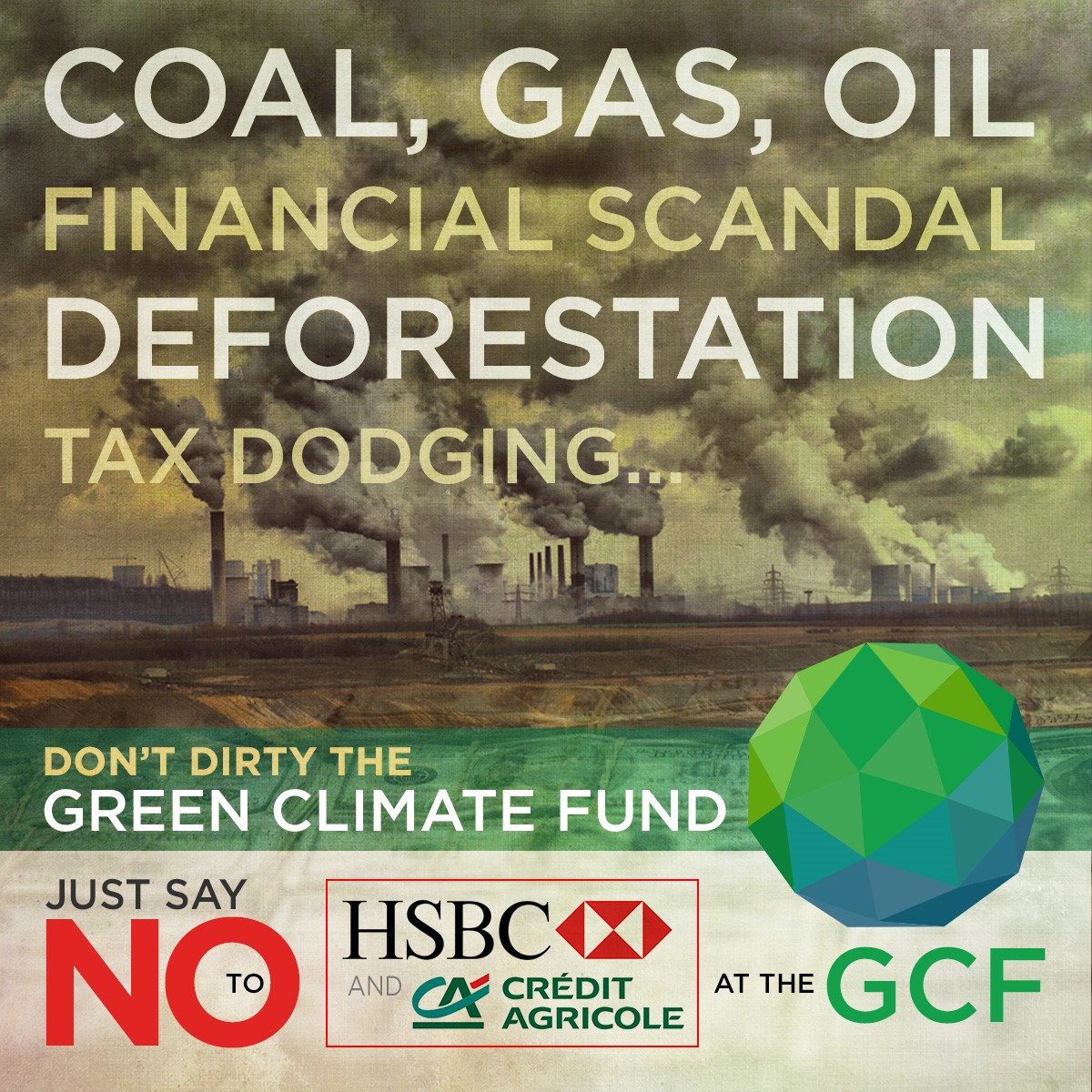

Either Wednesday or Thursday of this week, the Board of the Green Climate Fund will decide whether or not banking giants HSBC and Credit Agricole will become “accredited entities” of the GCF. Accredited entities are official partners of the GCF; they can receive and manage GCF funds.

Here are five simple reasons why the GCF Board should reject their applications for accreditation.

Number 1: Scarce public finance must be used to support communities in developing countries, not to subsidize Big Banks.

Number 2: HSBC and Credit Agricole would pose unnecessarily high risk to the fund. HSBC in particular is deeply embroiled in massive financial scandal. While we firmly believe that the Board should not accredit HSBC due to its poor record on climate pollution, environmental and social harm, and human rights, it would be premature for the Board to make a judgment on the fiduciary and reputational risks that accrediting HSBC would entail for the GCF before the public release of a report by an independent monitor overseeing the clean-up of HSBC’s massive money laundering. The Accreditation Panel (which assesses accreditation applicants) must fully review the report’s findings in order to perform its due diligence.

Number 3: Accrediting HSBC and Credit Agricole would be inconsistent with the Paris Agreement. HSBC and Credit Agricole provided US$7 billion and US$9.5 billion, respectively, to the coal industry between 2009 and 2014. Their coal financing does not show a clear downward trend, not to mention oil and gas. Any private sector partner of the GCF must have a credible strategy in place to make its entire portfolio and operations consistent with keeping global temperature rise to well below 2 °C, let alone 1.5 °C.

Number 4: The accreditation of Credit Agricole and HSBC would represent a clear double standard. It seems highly unlikely that the Board would accredit a direct access entity from a developing country with a track record of immense financial scandal like that of HSBC. We can even see a demonstration of this double standard in the current batch of applications. The Ministry of Finance and Economic Cooperation of Ethiopia (MOFED) was downgraded from large to small by the Accreditation Panel because of a lack of track record. If the lack of a track record is a problem for MOFED, why is it that a really bad track record is not a problem for the likes of HSBC?

Number 5: Some Board members have said that because the Board approved Deutsche Bank as an accredited entity back in July, it must also approve HSBC and Credit Agricole now. Why repeat the same mistake twice? The fact that you made a mistake once is not a justification for repeating it. In fact, as a learning institution, the Board is obligated to correct its course.

For further background, including references for all the information listed above, please see the civil society statement signed by 172 groups worldwide, No to HSBC and Credit Agricole at GCF.